That’s why most homeowners end up staring at a cracked backsplash or a leaking roof, realizing their savings account isn’t nearly as deep as their ambitions. You start out thinking you can handle a weekend of DIY, but then you find out the cost of quality lumber or a professional plumber isn’t something you can just “squeeze in” between work shifts.

It’s a common trap. You want the kitchen upgrade or the new deck, but you don’t want to drain your entire emergency fund. That’s usually when the conversation shifts toward debt, specifically personal loans or specialized home improvement financing.

Most people assume they have to deal with a massive, bureaucratic headache to get the cash. They imagine weeks of paperwork and mountains of documentation just to fix a leaky roof.

But things are changing. The gap between “I need money” and “the money is in my bank account” is closing faster than it used to. Some lenders now offer same-day credit decisions for most applicants, which changes the math when a contractor needs a deposit by Friday.

Comparing the Loan Landscape

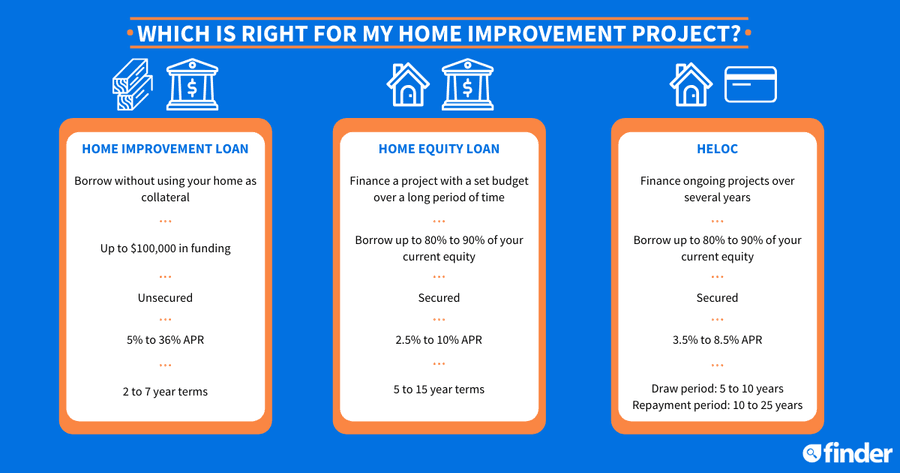

If you decide to go the personal loan route, you aren’t just looking at one type of product. There’s a wide spectrum of ways to borrow money to fix up your property. You can use a loan to pay contractors directly, or you can use it to cover the raw cost of materials if you’re doing the sweat equity yourself.

Some people prefer a lump sum. You borrow the entire amount all in one go. This gives you the freedom to start the project whenever you want, rather than waiting for a bank to approve incremental draws as you hit different stages of construction.

Wells Fargo offers home improvement loans that don’t charge an origination fee, a closing fee, or a prepayment penalty. That’s a big deal because if you finish your project early and want to wipe out the debt, you won’t get hit with a penalty for being responsible.

The math on these loans can be tricky depending on your credit score. You might see rates that look incredibly attractive on a brochure, but those are often reserved for people with pristine credit.

| Feature | Personal Loan for Home Improvement | Home Equity Loan/HELOC |

|---|---|---|

| Collateral | Unsecured (usually) | Your Home |

| Tax Deductibility | Generally not deductible | Potentially deductible if used for home improvements |

| Approval Speed | Fast (days or hours) | Slow (weeks or months) |

| Loan Amounts | Typically $1,000 to $100,000 | Based on home equity |

Deciding between these options depends on your timeline and how much risk you’re willing to take. If you need a new roof immediately because the old one is failing, you probably don’t have three months to wait for an appraisal.

The Cost of Borrowing Your Equity

Not all debt is created equal. When you use a personal loan for a renovation, you’re essentially trading a monthly payment for convenience and speed. It’s a trade-off you have to weigh carefully.

The interest you pay on a personal loan is not tax-deductible. This is a big distinction from other types of financing, such as home equity loans, where the interest might offer some tax advantages if the money is used specifically to improve the home. I’ve seen many people get tripped up by this when they are calculating their long-term costs.

If you’re looking at a large-scale project, like a new addition or a swimming pool, the numbers get bigger. For these larger endeavors, a personal loan might offer more flexibility in how you spend the cash. You aren’t tied to a specific contractor or a specific list of materials; the money is simply yours to deploy.

The range for these loans is quite broad. You can find them for as little as $1,000 for a small repair or up to $100,000 for a major overhaul. Because these are often unsecured, the interest rates can vary wildly. You might see rates anywhere from 7% to 36% depending on who you are and how much the bank trusts you to pay them back.

If you’re currently navigating the financial side of homeownership, you might be looking for more specific advice on how to manage your debt through sites like texasloanstoday.com to see what your local options might look like.

But the real question is: do you actually need the full amount up front? Sometimes, a smaller, quick-access loan is better for emergencies.

- Immediate repairs: New roof, plumbing upgrades, or HVAC issues.

- Aesthetic updates: Painting, flooring, or new cabinetry.

- Value additions: New rooms, decks, or landscaping.

Navigating the Credit Hurdle

We need to talk about the elephant in the room: your credit score. If you walk into a bank with a “fair” or “poor” rating, the options available to you shrink significantly. Many people search for “no credit check” loans or “bad credit” options, but you need to be careful.

Low-credit options exist, but they come with a price, and I don’t just mean the interest rate. The interest rates on these products can be predatory, effectively making the renovation cost twice as much as the original quote.

And while the idea of a “zero interest” loan sounds like a dream, they are incredibly rare and usually come with very strict requirements or short repayment windows. Most of the time, if someone is offering “zero interest,” there is a massive catch involving fees or a very specific, narrow window of time to pay it back.

Navy Federal Credit Union suggests that personal expense loans are a good choice when you need money quickly for smaller projects or emergencies. This is often the sweet spot for many homeowners. If you have an unexpected plumbing disaster, you don’t want to be negotiating with a mortgage lender; you want a solution that works as fast as the water is leaking.

If you need to move fast, you might find that a credit union offers more flexibility than a national bank. They tend to look at the person more than just a number on a screen, though they still demand a reasonable level of stability.

Making the Final Call

Before you sign anything, look at the total cost of the loan, not just the monthly payment. A low monthly payment might look great on your budget today, but if that loan term is six years long, you are paying a staggering amount in interest over time.

Ask about the fine print. Is there an origination fee that gets taken out of the loan before you even see it? If you borrow $10,000 but only $9,500 hits your account because of fees, you still owe the bank $10,000.

It is also worth checking if the lender allows for early repayment. If you get a bonus at work or a tax refund and want to kill the debt early, you shouldn’t be penalized for it. As mentioned with Wells Fargo, the absence of prepayment penalties is a massive win for the borrower.

You also need to be honest with yourself about the project’s value. If you are borrowing $50,000 to put a high-end kitchen in a house that is only worth $200,000, you might not see a return on that investment. You are essentially betting that the kitchen will increase the home’s value by at least the cost of the loan plus the interest.

If you’re doing it because you love the kitchen, that’s a lifestyle choice. If you’re doing it because you think it’s a “smart investment,” do the math twice.

Don’t let the excitement of a new floor or a fresh coat of paint blind you to the reality of the debt you’re taking on.

FAQ

What are the typical home improvement loan rates?

Interest rates vary based on your credit score and the lender, but they generally range from 6% to 36% for personal loans.

Can I get personal loans for home improvement with bad credit?

Yes, many lenders specialize in bad credit loans, though you will likely face significantly higher interest rates and lower borrowing limits.

Are there government loans for remodeling a home?

Yes, programs like FHA 203(k) loans allow homeowners to finance renovations by adding the costs to their mortgage.

Do personal loans for home improvement with no credit check exist?

While some lenders offer 'no credit check' options, they are often predatory with extremely high APRs and small loan amounts.

Are there zero interest home improvement loans?

True zero-interest loans are rare, but some lenders offer 0% introductory APR periods for the first 6 to 18 months on certain personal loans.